What is Blockchain Technology? The core technology powering a new future of finance has never been stronger, despite the wrath of uncertainty and volatility within bitcoin markets.

Did you know that roughly 16% of Australians currently hold some form of cryptocurrency? That’s about the same as having three or four of your work colleagues in your office building. The true technology underpinning Bitcoin and Dogecoin, however, is Blockchain, which is not widely known.

One of the most statistically volatile and risky asset classes, cryptocurrency has big bear and bull markets that cause scepticism about its veracity and legitimacy during times of significant decline, such as June 2021.

Nonetheless, the Blockchain technology itself has only expanded during this time.

What is Blockchain Technology?

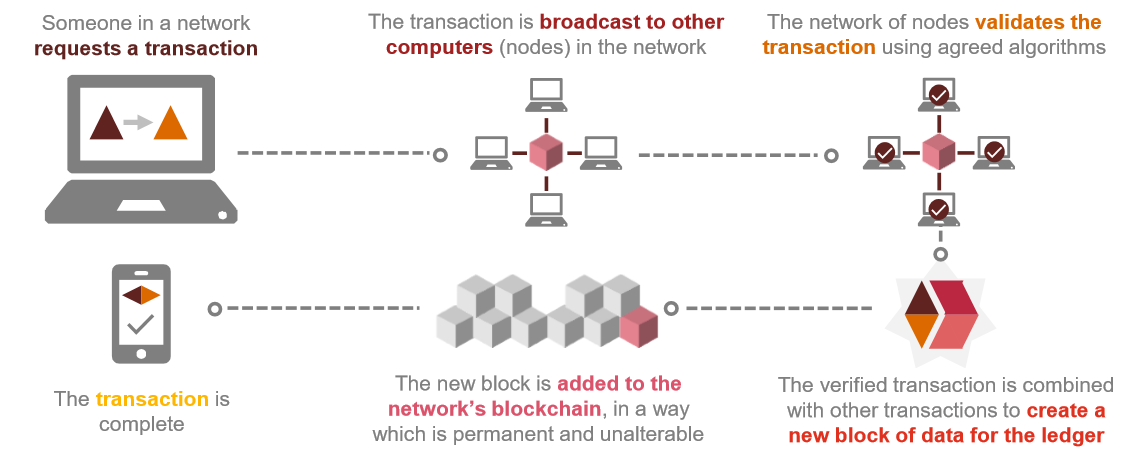

Blockchain technology is a method of documenting transactions in a way that makes tampering, hacking, or cheating exceptionally difficult, if not impossible.

Simply explained, a blockchain is a shared digital ledger of all the transactions that have ever taken place throughout the whole blockchain network of computers. Every time a new transaction takes place on the blockchain, the relevant information is updated to all of the participants’ ledgers and a new block is added to the chain.

Distributed ledger technology (DLT) refers to a system in which several users collectively administer a decentralised database. Blockchain technology is a form of distributed ledger technology (DLT) in which transactions are recorded using a hash that cannot be altered.

Why is Blockchain Technology Important to Us?

In today’s world, information transfer is essential to every aspect of life. Whether you’re surfing the web for your favourite social media site, online grocery shopping, or conducting financial transactions, the internet is always there for you.

Blockchain technology aids in the validation and tracking of multi-step transactions. It has the potential to hasten the processing of data transfers, lower compliance costs, and ensure the safety of financial dealings. The provenance of a product or service can be determined by the use of a contract.

Blockchain technology also has use in voting platforms and land record keeping. Particularly important and controversial is the tractability of online voting systems. Counts may not be necessary after this.

What is Decentralised Finance and its Connection to Blockchain Technology?

Decentralised finance is an alternative to centralised banking that is safer, more transparent, and more efficient. If we can do away with reliance on centralised banks, we can create a monetary system that is both more open and more trustworthy.

The lack of a centralised system in the United States makes it difficult for the government to control the flow of information.

There will be no overdraft fees, no wire transfer fees, and no need to wait for a transaction to be validated during trade hours, all of which will make financial management substantially cheaper and more efficient.

Ethereum, the second largest cryptocurrency exchange, already serves as a framework for the development of other blockchain applications (Ethereum’s cryptocurrency is used to finance processing fees) and hosts the vast majority of DeFi-related financial services.

By utilising decentralised applications, or dApps, blockchain technology and smart contracts enable real-time transactions between two or more parties without the use of an intermediary or additional costs.

How will Blockchain Technology be Adopted and what could it Mean for the Economy?

Adoption of blockchain technology will be slow, like that of many other technologies in the past, like the internet and mobile phones, and technologies in the present, like crypto currencies and electric cars.

Blockchain technology allows for new methods of organising economic activity, cuts down on the time and money spent on middlemen, and increases confidence in a company’s overall economic structure. While the potential for blockchain technology to disrupt established industries and inspire new ones is undeniable, its use and influence are still in the exploratory stages.

This technology has the ability to revolutionise any sector, making the world a better place by allowing individuals to keep more of the money they earn. For instance, the music business is a total failure from the artists’ perspective. The major labels used to take the lion’s share of the value that they offered.

And then along came the tech corporations and snatched off all the value, leaving the artists and musicians with scraps. What if the new music industry was a blockchain-based distributed software where I, as a songwriter, could upload my song and attach a smart contract dictating how it may be used?

Blockchain technology that enables secure data transfer and high levels of confidence in the veracity of any data you choose to safeguard.

NFTs make it possible for vendors to confirm the legitimacy of a digital asset by referencing its immutable blockchain record. When you purchase an NFT, your transaction is recorded on the distributed ledger and can be checked to prove who actually owns the tokens.

Blockchain technology aids the valuation of digital art and collectibles by allowing its authenticity to be verified, just like their physical equivalents. In theory, this allows artists to keep their work valuable by collecting royalties from people who make copies of their digital works.

This shows that a digital economy can exist alongside digital property rights, which may seem counterintuitive to those of us who do not place a high value on such things. He explains that this is because it provides you the exclusive right to declare, “I own and control this piece of the digital economy.”

One of the most significant applications of blockchain technology could be the safe and reliable transmission of sensitive personal information.

Just think about the implications if your financial data was kept in a blockchain.

A blockchain ledger might be used to swiftly and securely verify the authenticity of a new account you open with a financial institution or a transfer of information between institutions. That might be a great approach to cut down on wasteful spending and fraudulent activity alike.

As a result, there is a growing interest in the adoption of blockchain technology. A blockchain-based election would benefit from a permanent voting record that cannot be tampered with after the fact.

Blockchain technology could help businesses keep more precise stock records. With improved supply chain transparency, blockchain may potentially assist customers in making more knowledgeable purchasing decisions.

This technology has the potential to aid food distributors in tracking down recalled items, or to help shoppers steer clear of products made using abused workers.

Why Should Blockchain Technology Matter to Me?

Blockchain technology is not a magic bullet that will solve all of your company’s or industry’s cost and efficiency issues, and businesses should be extremely cautious about how the technology can be integrated into and used in the various sections of the business.

Even while mass commercialisation of blockchain sites and apps may not happen for a while yet, it is important to not discount blockchain’s influence on all industries, both now and in the future. Every existing transactional platform and procedure is likely to be enhanced or replaced by a blockchain-based solution.

If companies and industries do not want to fall behind, they will need to find a way to escape the innovator’s dilemma and make changes from the inside out. This will allow them to satisfy the requirements of their customers both today and in the foreseeable future.